Prev Post

Maharashtra Makes Tentative Layout Approval Mandatory Before Land MeasurementWestcon of the Solitaire Group Pays ₹129 Crore to Purchase Almost 10 Acres in Wagholi, Pune

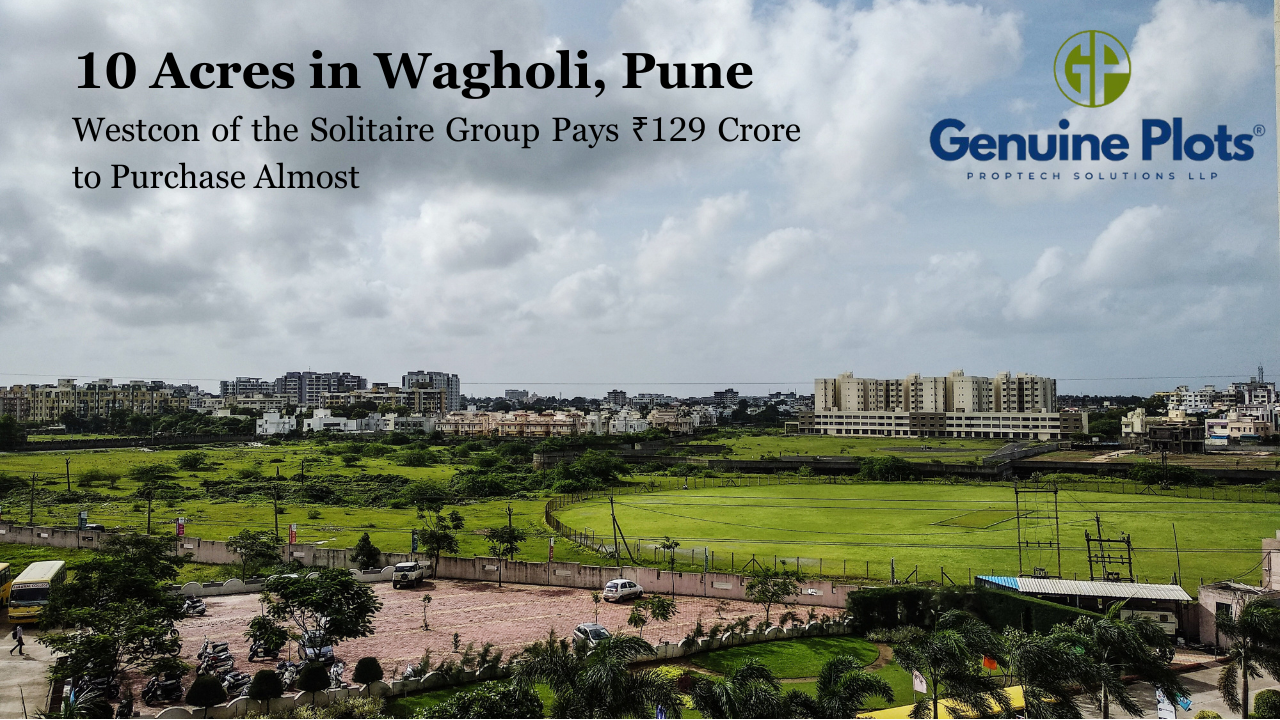

Westcon Spaces Pvt. Ltd., a division of Solitaire Group, has paid more than ₹129 crore for nearly 10 acres (roughly 4 hectares) of land in Wagholi. The acquisition was completed through four separate transactions on February 6, 2025. A 4-acre plot was bought for ₹40 crore, and the largest parcel, which was about 5 acres, was bought for ₹50 crore. For ₹28 crore and ₹11 crore, respectively, two smaller parcels of 0.5 acres were purchased. The premium nature of the location was demonstrated by the several crores in stamp duty payments for all four transactions.

Why Wagholi?

Situated in Pune's quickly expanding northeastern corridor, Wagholi has become a popular residential and business area. Both developers and homebuyers find it appealing due to its close proximity to the Kharadi IT hub, enhanced infrastructure, and improved connectivity.

Significant urban development is taking place in the area, and a number of real estate companies are making large investments to capitalise on the potential for future growth.

This purchase is indicative of a larger pattern of aggressive land banking by leading developers in India's largest cities. More than 2,000 acres were covered by land deals in the top eight urban markets in 2024, up 47% year over year, according to CBRE India. Pune continues to be one of the busiest real estate markets due to migration inflows, infrastructure improvements, and IT-led jobs.

Strategic Move for Solitaire Group

Solitaire Group made a calculated decision to expand the scope of its Pune project portfolio by purchasing the Wagholi land. The large plot of land can accommodate large-scale mixed-use, residential, or commercial projects that would help the organisation achieve its expansion objectives and increase its exposure in high-potential locations.

With this acquisition, the developer is well-positioned to meet the rising demand for quality housing and integrated living spaces in one of Pune’s fastest-evolving neighbourhoods.

Source:Hindustan Times

Roadmap to Double MMR’s GDP by 2030- Sectoral Opportunities & Challenges

MMR hopes to double its GDP by 2030, achieving a stronger and more competitive $300 billion urban economy.

This requires significant private investments, as well as the creation of millions of new jobs in new sectors.

Service as the Growth Driver

The objective is to become a global services hub.

Expansion to sectors like IT, fintech, banking, media, and global capability centers.

New job clusters being developed in Thane, Navi Mumbai, Kalyan, and Panvel.

Housing & Urban Upgrade

A larger push for affordable housing and redevelopment.

Goal: Ease pressures on South Mumbai and promote growth in the region.

New townships, as well as micro-cities, will be established to accommodate

Infrastructure as the Backbone

Massive upgrades to metro networks, expressways, rail corridors, and multimodal hubs.

Improved mobility → higher productivity, better connectivity, and new real estate hotspots.

Ports, Logistics & Manufacturing

Strengthened logistics chains through port modernisation, industrial parks, and warehousing zones.

Diversifies MMR beyond a finance-led economy.

Tourism & Lifestyle Economy

Development of coastal, heritage, and leisure circuits to improve tourism revenue and job creation.

Main Challenges

Mobilising private capital

Land + Environmental Constraints

Making sure the infrastructure keeps pace with economic growth

Why It Matters

MMR is in the midst of a rapid expansion phase—more jobs, better housing, increased connectivity, and increased economic opportunities.

MMR 3.0: Korea Joins Hands with Mumbai to Build the Next-Generation Smart City

A major step toward building a futuristic Mumbai was taken as MMRDA strengthened its partnership with South Korea to accelerate smart-city development across the Mumbai Metropolitan Region. Dr. Sanjay Mukherjee, IAS, Metropolitan Commissioner of MMRDA, highlighted that this collaboration will help shape “Mumbai 3.0”—a vision of a modern, innovative, and globally competitive metropolis.

During the India Global Forum 2025, senior Korean government officials, urban planners, and industry leaders met with MMRDA to explore opportunities for technology-driven urban development. The focus was clear: combine Korean smart-city expertise with Mumbai’s large-scale infrastructure push.

Key Focus Areas of the Partnership

Learning from world-class Korean smart cities such as Incheon and Songdo

Developing smarter, greener mobility solutions in the Mumbai region

Introducing AI-based city management systems for safety, traffic, and public services

Creating innovation zones, logistics hubs, and fintech clusters

Bringing more global investments into large infrastructure and urban projects

Launching joint pilot projects under the Global Twin Cities Platform

Mumbai recently joined this international platform through an MoU with the World Smart Cities Forum, giving the city access to global best practices and advanced technology frameworks.

A Strategic Step Toward a Future-Ready Mumbai

During the India Global Forum 2025, top Korean officials, smart-city experts, and industry leaders met with MMRDA to strengthen cooperation in the areas of urban planning, digital innovation, mobility, and city management.

Critical Facets of the India–Korea Partnership: MMR 3.0

Strategic Collaboration:

On this basis of the partnership, the MoU with WSCF brought Mumbai into the Global Twin Cities Platform, exchanging advanced global best practices and jointly undertaking smart city initiatives.

Core Objective :

Upgrade the Mumbai Metropolitan Region to a globally benchmarked smart city with high-quality urban planning, digital public infrastructure, and efficient future-ready mobility systems.

Adoption of Korean Expertise:

These include studies on the introduction of Intelligent Transport Systems, smart mobility solutions, and modern city management technologies that are inspired by the successful Korean Smart Cities: Incheon and Songdo.

MMR 3.0 Vision:

The initiative intends to go beyond basic smart-city features, building a deeply integrated, sustainable, innovative, and citizen-centric urban ecosystem. The aim is that this ecosystem will enhance the quality of life, enable better public services, and contribute to economic growth.

The India–Korea smart-city alliance marks a new chapter in Mumbai’s development story. By combining Korea’s proven technological expertise with Mumbai’s expansive infrastructure push, MMR 3.0 promises a cleaner, smarter, greener, and better-connected future for millions of residents.

The Mumbai Metropolitan Region is no longer expanding outward—it’s re-engineering itself.

With MMR 3.0, the region is entering a decisive phase where infrastructure, decentralisation, and long-term economic planning converge. For investors looking at 2026 and beyond, this isn’t just another real estate cycle—it’s a structural shift.

This guide breaks down where the opportunities lie, what’s driving them, and the risks you must factor in before investing.

What Exactly Is MMR 3.0—and Why It Matters to Investors

MMR 3.0 is a long-term regional transformation vision focused on:

Decongesting Mumbai city

The creation of diversified economic and residential hubs

Building transit-led development corridors

For real estate:

Growth is no longer South Mumbai-centric.

Peripheral locations increase in value with the back of infrastructure

Early movers tend to benefit more.

Key Investment Opportunities Under MMR 3.0

- Emerging Growth Corridors

MMR 3.0 is driving the development of a better-connected, though underpriced, region aggressively.

Zones: Investor-watch

Panvel-Ulwe-Dronagiri

Kalyan – Dombivli – Shilphata belt (Metro + Suburban rail improvement)

Virar – Vasai – Palghar (Affordable Housing + Rail expansion)

Karjat – Khopoli – Neral (Second home and Plotted Development Demand)

Why they matter:

Such locations are shifting from "future potential" to functional zones of live infrastructure, and as per historical reports, it is expected that price appreciation will take place in phases.

- Infrastructure Led Appreciation (The Real Game Changer)

Unlike speculative boom phases, MMR 3.0 has a foundation in execution-based infrastructure:

Metro lines extending deep into the suburbs

Multimodal transport hubs

Road corridors such as Virar-Alibaug and Panvel

Navi Mumbai International Airport ecosystem

Investor Insight:

Property prices go up before project completion; they do not go up after completion. 2025-26 represents a sweet spot for entry into locations where connectivity is perceivable but not yet fully priced in.

- Plotted Developments & Land Parcels

One of the strongest undercurrents of MMR 3.0 is the revived interest in:

NA bungalow plots

Gated plotted communities

Invest in mixed-use land

Why plots are gaining traction:

Lower cost of entry compared to apartments within the city.

Flexible construction schedules

Higher long-term appreciation in Infrastructure-driven belts

Increasing demand for second homes and low-density living

The trend is particularly true in Navi Mumbai outskirts, Karjat, Khalapur, and Vasai-Palghar regions

- Rental Yield & End-User Demand in Decentralised Business Hubs

While MMR 3.0 facilitates the proliferation of distributed job centres, not everybody is employed in either BKC or Nariman Point.

Hot Rental Demand Zones:

In proximity to Information Technology Parks, Logistics Parks, and Industrial Clusters

Locations with metro or expressway connectivity

Townships that offer work-life ecosystems

For investors, it means stable rental income and capital growth, particularly in mid-segment housing.

Risks Factor you must know

- Infrastructure Timeline Risk

Not all projects were at the same stage of development.

Smart investor move:

Plan your investment in areas where construction activity is already in progress, as opposed to merely proposed.

- Oversupply in Certain Micro-Market

Some pockets may see:

Too many similar apartment configurations

short-term price stagnation

Competitive Rental Market

Mitigation

Rather than focusing on the costs of launch alone, focus on connectivity, quality of layout, and liveability:

- Regulatory & Land Title Complexity

Especially relevant for:

Plots

Agricultural to NA Converses

Peripheral developments

Rule of thumb:

Title clarity, RERA registration, and zoning clearances are non-negotiable.

- Speculative Hype over “Third Mumbai”

Although the vision is massive, not all parcels around it could be equally impacted.

Reality check:

The areas of value will be concentrated around transport nodes, clusters of economic activity, and utility-ready zones.

2026 Investor Strategy: The Way to Play MMR 3.0 Wisely

Think 5–10 years, not quick flips

Prioritise infrastructure visibility over launch hype

Diversify between apartments, plots, and emerging nodes

Balance affordability with future connectivity

Work with local experts who are familiar with the area and the processes involved in obtaining necessary approvals and zoning

Final Take: Is MMR 3.0 Worth Investing In?

For informed investors, it may provide:

Entry into future growth hubs

Infrastructure-secured appreciation

Opportunities Beyond Saturated City Limits

However, it depends on the timing, the precision of the location, and due diligence.

Can NRIs Buy Plots in India? 2026 Rules, Restrictions & New Tax Ease Explained

For many NRIs, owning a piece of land back home is more than an investment—it’s an emotional anchor. A future home, a retirement plan, or simply a long-term asset that grows in value over time. But before taking that step, it’s essential to understand what the law actually allows.

Surprisingly, the rules for NRIs are more straightforward than most people think—especially after the latest Budget 2026 announcement that has simplified one of the most troublesome tax requirements.

Let’s break everything down in simple terms.

So, Can NRIs Buy Plots in India?

Yes, absolutely.

NRIs are free to buy:

Residential plots

Commercial plots

Apartments and other built homes

There’s no need to approach the RBI for approval, and there’s no cap on the number of properties you can own.

Where the law draws a hard line is with:

Agricultural land

Plantation estates

Farmhouses

These cannot be bought directly, no matter where the NRI is living. They can only be inherited or received as a gift.

A Big Change in 2026: No More TAN Requirement

If an NRI sells property in India, the resident buyer is required to deduct TDS.

Until now, this process involved the buyer getting a Tax Deduction Account Number (TAN)—a step that confused most people and often delayed the deal.

Starting October 1, 2026, this requirement disappears.

Buyers can simply use their PAN to deposit the TDS.

No extra numbers, no extra paperwork.

This small change will make NRI transactions much smoother and quicker.

How NRIs Are Expected to Pay

All payments for property—whether a plot or a ready home—must come in Indian Rupees.

NRIs generally use these accounts:

NRE

NRO

FCNR

Funds can also be transferred from abroad directly through banking channels.

Cash is not allowed, and foreign currency must not be handed over physically.

Loans from Indian banks are permitted too, as long as the funds flow through regulated accounts.

Using a Power of Attorney (POA)

Most NRIs can’t fly back to India for every signature or document.

The law understands this.

A Power of Attorney can handle:

Registration

Agreement signing

Possession formalities

Signing the POA at an Indian Consulate or before a recognized notary abroad is enough. The document just needs to be stamped or adjudicated once it reaches India.

What Happens When an NRI Sells a Plot?

Repatriation is allowed, but with limits.

You can send up to USD 1 million per financial year out of India, provided:

Taxes are cleared

The original purchase payment can be proven

Documents like the sale deed are in order

A chartered accountant will typically handle the compliance for repatriation.

Things NRIs Should Watch Out for Before Buying

- Check if the plot is truly “residential”

Some plots are marketed as residential but may still be listed as agricultural on government records.

Always verify land conversion documents.

- Check RERA registration

Most plotted developments are legally required to get RERA approval.

This will also protect you against delayed handovers or disputed layouts.

- Verify the seller's title

Land ownership is a sensitive issue in India. One has to check:

Title chains

Certificates of Encumbrance

Demarcation and layout approvals

- Citizenship restrictions

If the NRI is a citizen of Pakistan, Bangladesh, China, Afghanistan, Sri Lanka, Iran, Nepal, or Bhutan, they must obtain prior RBI approval before buying anything.

Why Many NRIs Prefer Plots Over Built Property

Compared to apartments, plot investments offer:

More freedom to build later

Higher appreciation in fast-growing cities

Lower maintenance costs

Better long-term resale value

For NRIs planning eventual relocation or retirement in India, a plot can be a sensible first step.

Final Thoughts

Buying a residential plot in India as an NRI is not complicated. The legal framework is friendly, and with the 2026 tax update eliminating the TAN requirement, selling to or buying from an NRI will become even simpler.

Non-Resident Indians (NRIs) have always been major investors in Indian real estate. One of the most common questions they ask is whether they can legally buy residential plots in India.

The answer is yes—but with a few important conditions.

Can NRIs Buy Residential Plots?

Yes, NRIs Can Buy Residential Plots

NRIs are allowed to purchase:

Residential plots

Residential apartments, villas, and houses

Commercial property

They do not need prior permission from the Reserve Bank of India (RBI) for these purchases.

What NRIs Cannot Buy

NRIs are not permitted to buy:

Agricultural land

Plantation land

Farmhouses

However, they may inherit or receive these as gifts, but cannot directly buy them.

Payment Rules for NRI Plot Purchase

When buying a residential plot in India, NRIs must follow these payment guidelines:

Payments must be done in Indian Rupees (INR)

Funds must come through:

NRE account

NRO account

FCNR account

Or inward remittance from abroad

Payments cannot be made in cash

Home loans from Indian banks are also allowed for NRI buyers.

Documents Required

To complete the purchase, NRIs typically need:

Valid passport

PAN Card

Proof of overseas address

Recent photographs

Power of Attorney (if someone else handles registration)

Sale agreement and title papers (from the seller or developer)

Why Residential Plots Are Popular Among NRIs

NRIs prefer residential plots because:

They provide good long-term capital appreciation

Buyers can build a house any time they want

Plots allow for flexibility in their design and construction

Gated layouts and plotted developments provide secure options to invest

Checklist for NRIs Buying a Residential Plot

Before Buying

Confirm land classification – It must be non-agricultural and approved for residential use.

Verify title documents – Ensure the land is free from legal disputes.

Check developer approvals – Layout approval, land conversion, etc.

Review RERA registration (if applicable).

Plan your payment method through NRE/NRO accounts.

During Purchase

Sign the sale agreement.

Complete stamp duty and registration at the Sub-Registrar office.

Ensure property tax records are updated in your name.

After Purchase

Maintain property tax payments.

Keep copies of all agreements and receipts.

If selling later, follow NRI capital gains tax rules.

Repatriation of Funds (Selling Later)

If an NRI sells the residential plot in the future, the sale proceeds can be sent (repatriated) abroad, subject to:

Tax compliance

Limits on repatriation from NRO accounts

Proper documentation of original investment

Summary

NRIs can purchase residential plots in India, provided the land is not agricultural and the payments go through approved banking channels. Buying a residential plot can be safe and profitable, with assured returns for long-term investment or a future home in India, with proper legal check of documents.

Recent Posts

Tags

Bhunaksha,

genuine plots,

Land For Sale,

Maharashtra Bhunaksha,

plots for sale,

Gunthewari,

Gunthewari Land,

Gunthewari Rules,

Extract Documents,

Plots and Lands,

Saat Baara,

Extract Saat,

Baara Utara,

Jamabandi,

property tax payments,

Gram Panchayat,

lower prices,

non-agricultural land,

Lower Investment Cost,

Gram Panchayat lands,

Fresh Land Settlements,

Growing demand,

affordable homes,

genuine p,

legal Land,

bungalow plots,

Konkan,

Maharashtra,

Purandar,

Pune,

Karnataka,

Bangalore,

Farm Land,

Kolkata,

Rajarhat,

Indore,

Chhatrapati Sambhajinagar,

Aurangabad,

Mundhwa,

Agricultural Land,

Farmhouse Plot,

Rules And Penalties,

Residential Plots,

NA PLots,

Residential NA Plots,

Commercial NA Plots,

Animal Husbandry Land,

Tathawade,

Vahivat Land Maps,

Vahivat,

Indian Land Records,

Ownership Rights,

Red zone,

PCMC,

Dehu Road,

Land Registration Rules,

Land Investing,

Infrastructure Growth,

Land Ownership,

Land Encroachment,

Panshet Dam,

Varasgaon Dam,

Verified Land,

Plot For Sale,

Land Investment,

Verified Plots,

Land Acquisiton,

Hydrological Survey,

Invest In Land,

Verified Land Plots,

Panshet,

Khadakwasla,

Land Rules,

Dakhil Kharij,

Land Registry,

Property Onwership,

Clean Title Check List,

Property Verification,

Digital Registry,

Farm Plots,

Agro Property,

Land Value Growth,

Urban Expansion,

Senapati Bapat Road,

Registered Land,

Agricultral Plot,

Purandar Airport,

Safe Investment,

Secure Property,

Plot Buyers,

Approved Plots,

Land ROI,

NA Approved Plots,

NA Land,

Welspun One,

Logistic Park,

Talegaon,

PMC Bharat Mandapam,

Urban Development,

Lohgaon,

Close To Nature,

Gated Community Plots,

Buy Land VS Gold Investment,

NRI Investment,

Future Ready Living,

Trusted Plots,

Plot Investment,

Authentic Land,

Safe Land Buying,

Mumbai,

Premium Plots,

MMR Land Investment,

MMR Infrastructure,

Metro Connectivity,

Plots in Mahabaleshwar hill station investment,

Mahabaleshwar land prices and future growth,

Scenic residential plots in Mahabaleshwar,

Mumbai 3.0,

Mumbai 3.0 vs Mumbai 2.0,

Mumbai property investment,

Real estate investment in Mumbai,

Upcoming residential projects in Mumbai,

CIDCO plot auctions,

CIDCO auction Navi Mumbai,

Upcoming CIDCO plot auctions 2026,

CIDCO land auction dates,

Navi Mumbai plot auctions,

CIDCO plots in Navi Mumbai,

CIDCO plots in Kharghar,

CIDCO plots in Ulwe,

NMIA investment opportunities,

Mumbai 3.0 plotted development,

Mumbai 3.0 real estate,

Plots in Mumbai 3.0,

Land investment in Maharashtra,

Residential plots near Mumbai,

Land appreciation in Mumbai 3.0,

Residential land for sale in Mumbai 3.0,

Altamura NA Plots,

Altamura Nadar City,

NA Plots in Nadar City,

Nadar City Plots,

Plots in Nadar City,

YEIDA plots,

YEIDA plots near Noida Airport,

Noida Airport plots,

Jewar Airport investment,

Yamuna Expressway plots,

YEIDA plot scheme 2026,

Noida Airport real estate,

Zepto,

Zepto effect,

D2C brands India,

Urban consumer trends,

Marketplace evolution,

Urban infrastructure growth,

YEIDA Residential Plot Scheme,

Yamuna Expressway Plot Scheme,

YEIDA Residential Plots,

Yamuna Expressway Authority,

Noida Investment,

Residential Plots in Lucknow,

LDA Plots in Lucknow,

Lucknow Real Estate,

LDA Approved Plots,

Plots for Sale in Lucknow,

Lucknow Property Investment,

Land Investment in Lucknow,

Residential Land in Lucknow,

Buy Plot in Lucknow,

Lucknow Development Authority,

Maharashtra Fragmentation Law 2025,

Fragmentation Act Maharashtra,

Maharashtra land law update 2025,

Maharashtra land reforms 2025,

Land subdivision rules Maharashtra,

Maharashtra agriculture land purchase rules,

Agricultural land purchase restrictions Maharashtra,

Can non-farmers buy agricultural land in Maharashtra,

NA conversion process Maharashtra,

Collector permission for land purchase,

farmland prices in Nagpur,

agricultural land price in Nagpur per acre,

farmland cost in Nagpur Maharashtra,

Nagpur agricultural land investment,

per acre agricultural land rate in Nagpur,

Tukdebandi Law Maharashtra,

Maharashtra Fragmentation Act update,

Land subdivision law Maharashtra,

Agricultural land division Maharashtra,

Maharashtra land reform ordinance,

Plot registration Maharashtra,

Farmland prices Nagpur,

Nagpur agricultural land rates,

Farmland per acre Maharashtra,

Agricultural land price Nagpur,

Farm land cost Nagpur,

Nagpur real estate trends,

Land investment Nagpur,

Avani Farms,

Avani Farms Pune,

Farmland near Pune,

Farm plots for sale,

Agricultural land investment,

Gated farmland near Pune,

NRI agricultural land rules India,

Can NRI buy agricultural land in India,

FEMA rules for NRI property purchase,

RBI guidelines for NRI land investment,

NRI farmland investment India,

Agricultural land purchase by NRI,

Maharashtra Fragmentation Act,

Minimum plot size in Maharashtra,

Guntha rules Maharashtra,

Agricultural land division rules,

Minimum land area for sale in Maharashtra,

Legal plot size in guntha,

Guntha conversion rules,

NRI land purchase in India,

Can NRIs buy agricultural land in India,

NRI property investment India,

NRI buying residential land,

NRI real estate guidelines India,

Investment tips for NRIs in India,

Mutation Entry Process,

Land Mutation in India,

Property Mutation Process,

Land Ownership Transfer,

1 guntha na plot prices in pune 2026,

1 guntha plot price in pune,

na plots in pune,

residential na plots pune,

guntha plot rate in pune,

na plot investment in pune,

plots near purandar airport,

1 Acre Land Price in Pune,

Pune Land Rates 2025,

Pune Land Price 2026,

Pune Acre Land Cost,

Land Value Pune,

Agricultural Land Price Pune,

gated community plots in Hinjewadi,

Hinjewadi plots for sale,

residential plots in Hinjewadi Pune,

premium plots in Hinjewadi,

plots near Rajiv Gandhi Infotech Park,

land for sale in Hinjewadi Pune,

Pune property investment,

plots for sale in Pune below 5 lakhs,

Pune rural land investment,

gated plotting projects Pune,

MIDC growth corridor plots,

Residential plots for sale in Hinjewadi,

Plots in Hinjewadi Pune,

Land for sale in Hinjewadi,

Residential NA plots Hinjewadi,

Hinjewadi real estate trends 2026,

Nashik land investment,

Trimbakeshwar land for sale,

Simhastha Kumbh 2026,

Simhastha Kumbh 2027 real estate impact,

Trimbakeshwar property investment,

Land appreciation in Nashik,

plots for sale in pune,

types of plots in pune,

residential plots in pune,

agricultural land in pune,

villa plots in pune,

NRI agricultural land purchase India,

NRI property investment in India,

Agricultural land rules for NRIs,

NRI real estate investment India,

NA plot meaning,

what is NA land,

NA land in Maharashtra,

land investment guide,

NRI agricultural land in Telangana,

Telangana land laws for NRI,

Telangana real estate laws,

NRI investment guide Telangana,

Legal compliance for NRI property,

NRI farmhouse purchase India,

RBI guidelines for NRI property,

NRI land buying rules,

Godham Eco Village,

Godham Eco Village for NRIs,

NRI land investment in India,

Investment plots for NRIs,

Secure land investment India,

NRI property buying guide,

plots in Pune,

NRI buying property in India,

NRI guide to buying land in Pune,

NRI land investment in Pune,

NRI property documents checklist,

Maharashtra land reform 2025,

Maharashtra land laws update,

Agricultural land rules in Maharashtra,

Buying agricultural land in Maharashtra,

Non-agricultural land conversion Maharashtra,

Maharashtra agricultural land rules 2024,

agricultural land purchase in Maharashtra,

non agriculturist land purchase rules,

who can buy agricultural land in Maharashtra,

Maharashtra land laws for non farmers,

Guntha based land rules,

Minimum guntha rule Maharashtra,

Maharashtra land laws,

Maharashtra agricultural land laws,

farmland investment Maharashtra,

buying farmland legally in Maharashtra,

NA conversion rules Maharashtra,

agricultural land eligibility criteria,

Property Mutation in India,

Land Record Update,

Revenue Records,

Property Ownership Transfer,

Mutation of Property,

Farmhouse Plots Near Pune,

NRI Investment in Pune,

Pune Real Estate,

Plots for Sale Near Pune,

Luxury Farmhouse Plots,

Pune plot scams,

Plot buying checklist,

Legal verification for plots,

NA plot verification,

Plot buying tips Pune,

Godrej Properties,

Evora Estate Panipat,

Luxury plots in Panipat,

Premium land investment,

Residential plots in Panipat,

Lodha Developers,

Lodha Developers Q3 acquisition,

Lodha land parcels Q3,

Indian real estate news,

New residential projects India,

Real estate investment news,

Premium housing projects,

Srijan Group,

Kolkata Tech Park,

Commercial Real Estate,

Real Estate Investment,

Real Estate Deal News,

NRI investment in India,

NRI land investment,

Plots for sale in India,

NRI property investment,

Can NRI buy residential plot in India,

NRI land purchase rules,

Residential plots for NRIs,

NRI real estate investment,

NRIs buying property in India,

Can NRIs buy plots in India 2026,

RBI rules for NRI property purchase,

NRI land investment rules,

MMR 3.0,

MMR real estate 2026,

Mumbai real estate market,

Navi Mumbai investment,

Thane property market,

Mumbai property trends 2026,

Land investment in MMR,

Mumbai smart city project,

Korea Mumbai partnership,

MMRDA infrastructure projects,

Korean investment in India,

MMR GDP growth,

MMR economic roadmap 2030,

Mumbai real estate,

Public private partnership projects Mumbai,

Investment opportunities in MMR,

Mumbai Metropolitan Region,

Mumbai urban development,

MMR 2047 vision,

Mumbai infrastructure projects,

Navi Mumbai development,

Goa property investment,

Invest in Goa 2026,

Goa real estate market 2026,

Best places to invest in Goa,

North Goa property,

Property appreciation in Goa,

Goa plots for sale,

Commercial property in Goa,

Buy property in Goa,

YEIDA plots 2026,

Residential plots in YEIDA,

YEIDA new scheme update,

Plots near Noida International Airport,

Yamuna Expressway Authority plots,

YEIDA housing scheme details,

Lucknow land investment,

Property in Lucknow,

Buy plots in Lucknow,

Nashik plots for sale,

Kumbh Mela 2026 Nashik,

Land investment in Nashik,

Nashik property market 2026,

Plots near Kumbh Mela Nashik,

Residential plots in Nashik,

Upcoming projects in Nashik,

Property appreciation in Nashik,

Maharashtra land investment,

Nashik Kumbh Mela 2026,

Kumbh Mela investment opportunities,

Infrastructure development in Nashik,

Plots near Nashik Kumbh Mela,

High ROI land investment,

MIHAN,

MIHAN Nagpur,

Nagpur Real Estate,

Agricultural Land Nagpur,

Nagpur Property,

Plots Near In MIHAN,

Pune residential plots,

best areas to buy plots in Pune,

Pune land investment,

investment plots in Pune,

buy land in Pune,

real estate investment in Pune,

Godrej Plots Doddaballapur,

Doddaballapur plots for sale,

Plots in North Bangalore,

Godrej Properties plots,

Residential plots in Doddaballapur,

Investment plots near Bangalore,

Gated community plots Bangalore,

Premium plots in Doddaballapur,

plots in Mahabaleshwar,

Mahabaleshwar villa plots,

farmhouse plots in Mahabaleshwar,

land for sale in Mahabaleshwar,

bungalow plots in Mahabaleshwar,

hill station property investment,

agricultural land in Mahabaleshwar,

premium land in Mahabaleshwar,

Plots in Pune under 3 lakhs for sale,

Budget residential plots near Pune,

Low cost plots near Pune highway connectivity,

plots in Pune under 3 lakhs,

farmland plots near Pune city,

Investment plots near Pune under budget,

Residential land near Pune,

Godrej plots in Pune,

Premium plotted development by Godrej in Pune,

Residential land for sale by Godrej,

Premium plot by Godrej,

Plots for sale in Hadapsar Pune,

Residential plots in Hadapsar,

Investment plots in Hadapsar,

Gated community plots in Hadapsar,

Ready to build plots in Hadapsar,

1 Guntha plot in Pune,

1 Guntha plot in Pune for sale,

1 Guntha plots near Pune city,

Residential 1 Guntha land in Pune,

Clear title 1 Guntha plot in Pune,

1 guntha plot price in village,

village plot rate per guntha,

affordable 1 guntha land in rural area,

residential plot in village Pune,

farmland plot price per guntha,

Residential 1 Guntha plot near Pune city,

Investment plots in Pune 1 Guntha,

Clear title 1 Guntha land in Pune,

Agricultural 1 Guntha plot near Pune,

1 Guntha plot in Pune Katraj for sale,

Residential plot in Katraj Pune 1 Guntha,

Katraj Pune land for home construction,

1 Guntha NA plot in Katraj Pune,

Pune Katraj plot near highway connectivity,

Gated plot project in Katraj Pune,

NA plots in Pune under 10 lakhs,

Affordable NA plots near Pune city,

NA residential plots in Pune,

NA approved plots in Pune under 10 lakhs,

Investment plots in Pune under 10 lakhs,

Residential NA plots near Pune highway,

Best plots in Pune below 10 lakhs,

Premium villa plots in Pune,

Residential villa plots in Pune near city outskirts,

Luxury villa plots in Pune,

Gated villa plot project in Pune,

Villa plot site visit in Pune,

NA plots in Pimpri Chinchwad for sale,

Residential NA plots in PCMC area,

NA approved plots in Pimpri Chinchwad,

NA land with clear title in PCMC,

NA plots near Pune Mumbai Highway PCMC,

Godrej Villa Plots Doddaballapur,

Godrej plotted development Bangalore,

villa plots in North Bangalore,

premium villa plots Bangalore,

Godrej Properties plots Bangalore,

Brigade Plots Malur,

Brigade Malur plots,

plots in Malur East Bangalore,

investment plots in East Bangalore,

residential plots in Malur Bangalore,

Brigade Group plots Bangalore,

land investment in East Bangalore,

gated community plots in Malur,

prestige plots devanahalli,

prestige plots in devanahalli bangalore,

plots for sale in devanahalli,

prestige plots investment,

premium plots in devanahalli,

residential plots near kempegowda airport,

What is NA plot in real estate,

NA land meaning in property,

NA approved plotsDifference between NA and agricultural land,

Buying NA plots in Maharashtra,

NA plot vs agricultural land,

Plot prices in Mysore,

Mysore infrastructure projects,

Mysore property investment,

Land investment in Mysore,

Plot investment opportunities,

land buying guide in goa,

buy land in goa,

plots for sale in goa,

legal process to buy land in goa,

property in goa,

residential plots in goa,

Nashik Simhastha Kumbh Mela 2026,

Sadhugram expansion Nashik,

Maharashtra Kumbh Mela planning,

Nashik Kumbh Mela preparations,

tourism development in Nashik,

plots in Nagpur,

Nagpur plot investment,

land for sale in Nagpur,

residential plots in Nagpur,

golden rules before buying plots in Nagpur,

Nagpur land investment,

plot investment in Nagpur,

land investment in Nagpur,

plots for sale in Nagpur,

best areas to buy plots in Nagpur,

buying plots in Nagpur,

plot purchase checklist,

legal checklist for buying land,

documents required for plot purchase,

NA plots in Nagpur,

Tattvana,

Tattvana in Kamshet,

Moregaon Farmland Estates,

farmland investment Pune,

agricultural land investment,,

farmland for sale near Pune,

farm plots in Pune,

gated farmland projects,

agricultural plots Maharashtra,

open plot vs NA plot,

difference between open plot and NA plot,

what is NA plot in India,

open plot meaning in real estate,

NA land vs agricultural land,

residential NA plots benefits,

land investment in India,

buying NA plot vs open land,

capital gains on agricultural land,

rural vs urban agricultural land tax,

agricultural land tax rules India,

capital gains tax India property,

is agricultural land taxable,

rural agricultural land exemption,

urban agricultural land tax India,

Runwal Enterprises Alibaug township,

Alibaug real estate,

coastal real estate India,

township projects in Alibaug,

luxury properties in Alibaug,

Mumbai weekend homes investment,

Alibaug property investment,

isprava south goa,

ultra luxury villas in goa,

south goa real estate,

luxury homes in goa,

isprava projects goa,

premium villas in south goa,

land investment advisory services,

secure land investment,

real estate advisory services,

verified land deals,

investment plots near Pune,

land buying guide India,,

#KanpurRealEstate,

#KDAPlots,

#KanpurProperty,

#RealEstateKanpur,

#PropertyTrends,

Gokul Plots investment,,

real estate investment Gokul,,

plots with high appreciation potential,

smart land investment strategies,

plots for sale in North Bangalore,

land investment Bangalore,,

emerging areas in North Bangalore,

residential plots Bangalore,,

Bangalore real estate investment,,

North Bangalore property trends,,

plots near airport Bangalore,,

HUDA plots in Gurgaon,

HUDA plots in Faridabad,

residential plots Haryana,

HUDA approved plots,

plots for sale in Gurgaon,

plots in Faridabad investment,

Prestige Marigold plots,,

Bangalore plotted developments,

land investment Bangalore,

best plots in North Bangalore,

#PlotsForSaleInNellore,

#NelloreRealEstate,

#NellorePlots,

#RealEstate2026,

#PropertyInvestment,

#NelloreProperty,

#AndhraPradeshRealEstate,

GMADA E Auction 2026,

GMADA plots Mohali,

plots in Mohali for sale,

GMADA Mohali auction process,

buy plots in Mohali,

Punjab property investment,

GMADA scheme 2026,

Mohali real estate,

HSVP plots 2026,

HSVP plot investment,

HSVP plots Haryana,

land investment benefits,

residential plots investment,

government approved plots,

buy plot in New Chandigarh,

flats in New Chandigarh,

New Chandigarh real estate,

property investment in New Chandigarh,

residential plots in New Chandigarh,

apartments in New Chandigarh,

#WaveCityGhaziabad,

#GhaziabadPlots,

#PlotsInGhaziabad,

#NCRRealEstate,

#RealEstateInvestment,

#ResidentialPlots,

APIIC vacant plots,

APIIC plots for sale,

industrial plots in Andhra Pradesh,

commercial land for MSMEs,

startup investment plots,

APIIC industrial land,

HUDA plots,

HUDA plots investment,

property appreciation,

plot investment benefits,

high return property investment,

land appreciation,

#GDAPlotsInGhaziabad,

#PlotsForSaleInGhaziabad,

#ResidentialPlotsGhaziabad,

#InvestmentPlots,

#RealEstateGhaziabad,

#GDAApprovedPlots,

#BaliProperty,

#PropertyInBali,

#IndiansInBali,

#BaliRealEstate,

#InternationalPropertyInvestment,

buy plots in Sarjapur Road Bangalore,

plots in Sarjapur Road,

residential plots in Sarjapur Road,

land for sale in Sarjapur Road Bangalore,

investment plots in Bangalore,

plots near IT corridor Bangalore,

how Indians can buy property in Bali,

buy property in Bali for Indians,

Bali property investment,

property in Bali for Indian buyers,

Bali real estate guide,

foreign property investment Bali,

legal checks before buying property in Bali,

Indians invest in Bali property,

due diligence for Bali property,

Bali real estate for Indians,

Bali property legal verification,

verified farmland plots,

100% verified farmland plots,

farmland investment India,

legal farmland plots,

farmland plots for sale,

Konkan land investment,,

high-growth corridors Maharashtra,

land investment 2026,

plots for sale in Maharashtra,